Financial Aid Resources

Forms, guides, and information to help SVA students navigate federal aid, scholarships, loans, and tuition assistance.

View All FormsHere you can download forms, review our code of conduct, browse frequently asked questions, and access financial aid resources. You can also use this site to get recent updates and news related to financial assistance.

2026–27 FAFSA Reminder

You can file the 2026–27 FAFSA form online at studentaid.gov using your FSA ID login credentials to electronically sign, as early as October 1, 2025, using your 2024 tax information.

If you have any questions, please contact Financial Aid by email at fa@sva.edu.

Financial Aid Loan Entrance Counseling

The federally mandated loan entrance counseling is required for all students receiving a Federal Direct Stafford Loan or Federal Direct Graduate PLUS Loan for the first time at SVA. Students who received a Stafford Loan at a previous institution do not need to complete entrance counseling here.

Students must complete entrance counseling before any loan proceeds may be received. The counseling is an information session explaining the student’s rights and responsibilities regarding these loan programs.

Please refer to your SVA email account for correspondence from our office regarding your applicable entrance requirements. Questions? Contact us at fa@sva.edu.

Exit Counseling

The federally mandated Exit Counseling session(s) are required for all students who received a Federal Direct Stafford Loan and/or a Federal Direct Graduate PLUS Loan at SVA.

Exit Counseling provides important information you need as you prepare to repay your federal student loan(s). Please refer to your SVA email account for correspondence regarding your applicable exit requirements.

Questions? Contact us at fa@sva.edu.

Special or Unusual Circumstances

SVA Financial Aid recognizes that changes may occur in a student’s financial situation. While the FAFSA determines eligibility based on data from two years prior, a process exists to re-evaluate aid based on certain significant changes.

- Job loss due to cause or personal choice

- Standard living expenses (utilities, car payments)

- Mortgage payments

- Personal debt

- Bankruptcy

Change to Student Aid Index (SAI)

A change to the SAI could result in a change of eligibility for need-based awards, but is not guaranteed. Possible changes include:

- Loss or change of employment (not due to cause or personal choice)

- Child support change

- Death of parent or spouse

- Excessive medical expenses (must exceed 11% of adjusted gross income)

- One-time taxable income (IRA distribution, pension distribution, etc.)

Change to Cost of Attendance (COA)

A change to the COA does not result in a change to need-based awards. It increases the total budget to allow for an increase to PLUS and/or private loans only. Possible changes include:

- Childcare expenses for a dependent child of a student

- One-time purchase of a computer for educational use

If you meet one of the significant changes outlined above, contact your assigned financial aid advisor to schedule an appointment.

News & Updates

2026–2027 Federal Loan Update

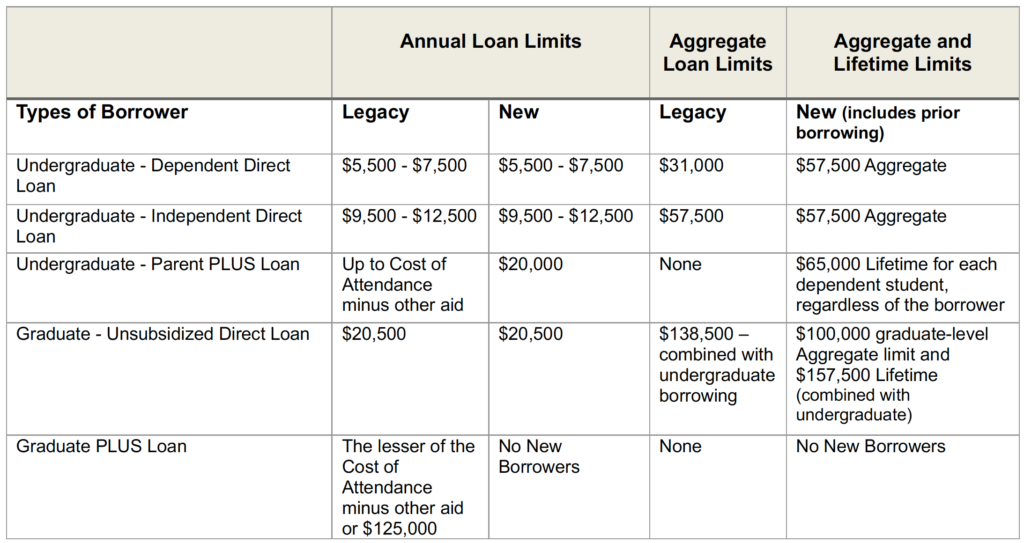

This document reflects SVA’s current understanding of new requirements as of April 24, 2026, and is subject to change. Congress passed the One Big Beautiful Bill Act (OBBBA) in July 2025, introducing several changes to federal student loan amounts effective July 1, 2026, including adjustments for less than full-time enrollment and changes to overall borrowing limits.

All federal Direct Loans, except Parent PLUS loans, will be subject to proration for less than full-time enrollment starting with the 2026–2027 award year, regardless of prior borrowing. This proration mirrors the ratio of enrolled credits to the full-time credit requirement for the academic year and is calculated before each semester disbursement.

Students must still be enrolled at least half-time to receive Direct Loans.

- New Borrower — A student with no federal loans disbursed (student or parent) for their current SVA program prior to July 1, 2026.

- Legacy Borrower — A student who received a federal loan (student or parent) prior to July 1, 2026, for a program in which they were enrolled as of June 30, 2026, and continues enrollment in the same degree program. This status can be maintained for the lesser of three academic years or the remaining program length. A student may lose legacy status upon withdrawal, academic break, change of credential level, or change of graduate program.

Legacy borrowers may continue to access existing loan program funding levels and provisions for the duration stated above, with the following exception: Graduate PLUS loan borrowers are limited to borrowing $125,000 per academic year under SVA borrowing limits, effective July 1, 2026. Legacy borrowers are subject to the new proration requirements for less than full-time enrollment, except Parent PLUS loan borrowers.

New regulations effective July 1, 2026 for borrowers who do not meet legacy requirements include:

- Undergraduate Direct Subsidized and Unsubsidized Loan annual amounts remain the same, subject to new proration for less than full-time enrollment.

- New lifetime loan limits and aggregate borrowing limits per credential level now apply.

- Repayment, refund, discharge, or cancellation after disbursement does not restore access under the new caps.

- Direct Parent PLUS Loan: limited to $20,000/year per student, $65,000 lifetime; not subject to less-than-full-time proration.

- Direct Graduate PLUS Loan is no longer available to graduate students.

- Graduate students: annual Direct Unsubsidized Loan limit of $20,500 remains; new aggregate limit for graduate-level borrowing is $100,000 (includes all prior graduate-level borrowing, not undergraduate). Subject to less-than-full-time proration.

- Total lifetime federal student loan cap: $257,500 (excluding Parent PLUS Loans). SVA students are limited to $157,500 (SVA does not offer programs qualifying for the additional $100,000).

- Within the $157,500 limit: $57,500 aggregate for undergraduate borrowing; $100,000 for graduate-level borrowing.